팀으로도 가능하지만 1. 친구가 없었고, 2. 경험상 그룹으로 진행하면 맡은 부분에만 집중하는 경향이 있어 전체를 아우를 수 있을 거란 기대, 3. 무엇보다 주말이라도 육아를 돕고자 조모임 왔다갔다 하는 시간을 아끼려고, 솔로팀으로 진행했다. 11개 팀 중 나 포함 두 명만 솔로팀으로 진행했다.

팀별로 지난 5년 이내의 인수건을 골라 진행하면 된다. 나는 BRIC 연재에서 몇 번 다룬 적 있는 농화학업계의 Bayer-Monsanto 건을 골랐다.

참고: 브릭연재 Bayer-Monsanto 관련 글

3개월 간 틈틈이 써왔고 지난 주말은 거의 책상에 붙어 있었다(이 글을 빌어 정말 육아에 고생이 많은 와이프님께 감사의 마음을 전한다).

리포트 전문을 옮긴다.

Caveat before reading:

1. I did not take the control premium into account. In reality, we should add the premium in a market acceptable range (e.g. 20%) on top of the business enterprise value derived from the Comparable company multiples (the control premium is already incorporated in the Comparable acquisition multiples and DCF methods). The concept is explained in another article in this blog: http://jinjjan.blogspot.com/2019/10/mba-notecorporate-financeintroduction_29.html

2. Suggested citation: Jin, Joon Yung, "Valuation of Monsanto Acquired by Bayer", December 9, 2019. Available at http://jinjjan.blogspot.com/2019/12/mba-case-studybayer-monsanto-acquisition.html

Valuation of Monsanto Acquired by Bayer

Dec 9th 2019

Jin, Joon Yung

Introduction

In the chemical

industry, years of 2015 to 2018 were monumental since big mergers and

acquisitions were significantly changing the landscape. Reminiscing on

their heydays back in early-mid 1990s, chemical companies sought sustainable

cash stream beyond their portfolios.

Materials for plastics and nylons had been commoditized and the market

was saturated by many players. The companies suffered from decreasing

revenues and profits in this competitive environment. Under the circumstance, most big players,

such as DuPont and BASF, already had begun to tap the agriculture business as

they saw this market was growing with various chemical applications.

Bayer is a global

chemical company with history of 150+ years founded in Germany with revenue of

$60 billion in 2015. It is well known with its

signature pharmaceutical product, aspirin. The German company had run it

business with pharmaceuticals and chemicals as its major sectors until it

acquired a Belgium agriculture company, Plant Genetic Systems in 2001 founding

Bayer CropScience. Bayer paid about $8 billion for Plant Genetic Systems

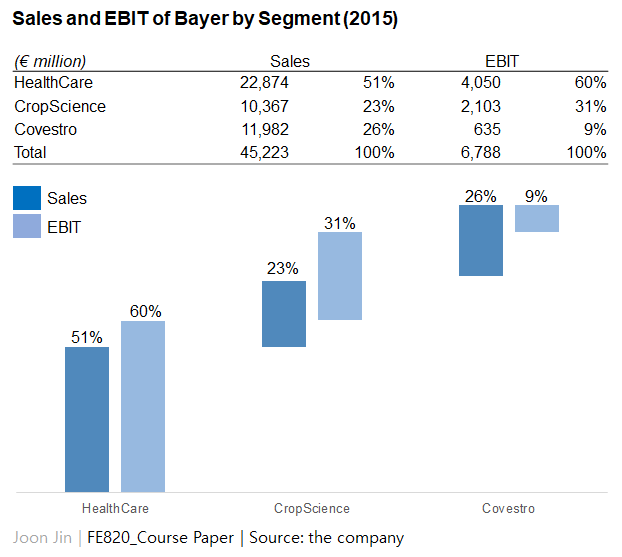

which was the largest amount for an acquisition in Bayer’s history. In 2016, the company defined themselves as a

life science company with three major segments, pharmaceuticals,

consumer-health, and crop science. Bayer’s CropScience segment consists

of crop protection and seeds, and in 2015 it represented 23% of Bayer’s net

sales and 31% of earnings before interest and taxes (EBIT) as shown in Exhibit

1.

Monsanto, an

agricultural biotechnology company, was founded in 1901 but established as a

sole agricultural company being divested from Pharmacia Corporation in

2000. The US company ran its international business with revenue of $15 billion in 2015 and it

represented the largest market share for seeds and crop protection

products. Its main products are glyphosate herbicide (RoundUp) and the

seed products conferred the glyphosate resistance by genetic engineering

(RoundUp Ready).

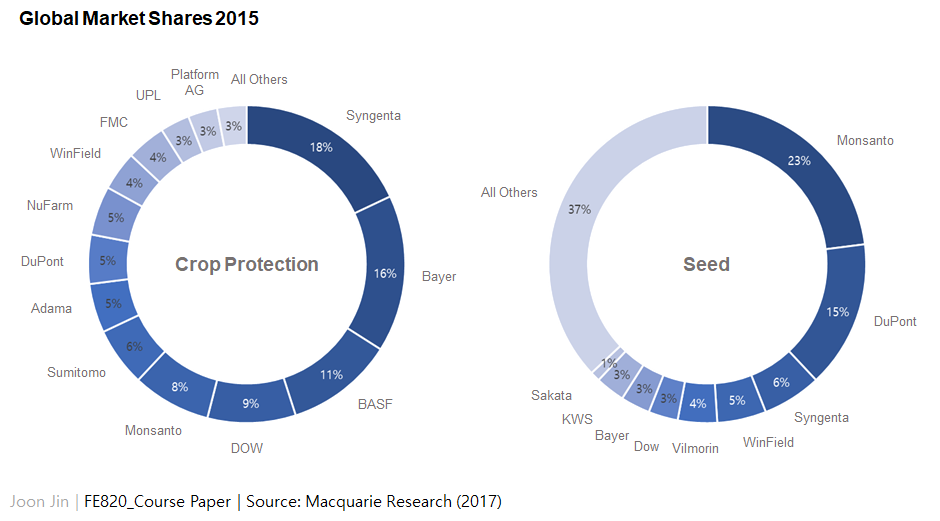

As of 2016, the

agriculture industry had witnessed several major consolidations (whether or not

they were successfully completed). The industry was already dominated by

a few big players (Exhibit 2), but the consolidation from 2016 occured even

among the big players (Exhibit 3). Monsanto had announced its intention

to acquire Syngenta, the 3rd largest agricultural company in sales, in 2015

(although the deal was failed), Dow Chemical and DuPont announced its merger in

same year which was completed in 2017, and ChemChina offered an acquisition

deal to Syngenta in 2016 which was also finalized in 2017. Amongst this

drastic change in the industry, Bayer also showed its intent to acquire Monsanto

in 2016 in the wake of the failure between Syngenta and Monsanto.

The German

chemical company made an unsolicited offer to buyout Monsanto in May

2016. The initial offer price per share in May was $122 but was increased

to $128 by September 2016 which is the actual price of the deal. Bayer

closed $63 billion Monsanto takeover in June 2018. The motivation of Bayer for the acquisition

might be to keep the competitors away from the largest agricultural company to

secure and increase the market share in the industry. The crop protection

(chemical products such as pesticides or herbicides) had shown the strong

business activity while its seeds and traits business had relatively not

(Exhibit 2). Monsanto was an appropriate

company to bridge the gap since it possessed the front-running biotechnology

business in agricultural industry across the world. In addition, they

were both paving ways to digital farming with data platforms and the merger

could provide them with a consolidated platform. On top of that, they were confident that the

alliance between European and American companies should give them geographical

merits such as diversified distribution channels, world-wide presence, and

dealing with regulatory affairs in different countries.

In this study, I

valuated Monsanto as of 2016 with three different methodologies: Comparable

company multiples, comparable acquisition multiples and discounted cash

flow. By doing this, I could compare the figures with the real dollar

amount Bayer ended up paying, then could conclude whether or not it was in a

reasonable range.

Results

Methodology 1:

Comparable Company Multiples

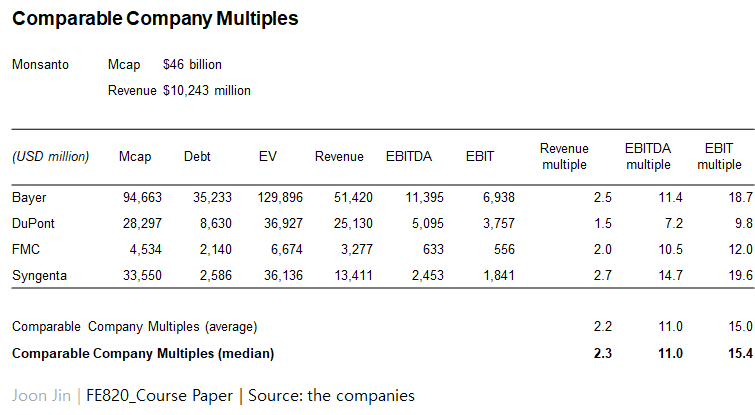

To get the comparable company multiples, I

used Monsanto’s peer group companies as of the end of fiscal year 2015.

Since the agriculture industry had been consolidated by a few big

chemical/biotechnology players as described above, I used four (4) companies

which possessed relatively similar size in terms of sales and market

capitalization with Monsanto (Exhibit 4). The revenue multiples ranged

from 1.5 and 2.7, did the EBITDA multiples from 7.2 and 14.7 and the EBIT

multiples ranged from 9.8 and 19.6. The median

multiples were 2.3, 11.0 and 15.4, respectively. The financial results

from operating of Monsanto on the annual report 2015 showed the sales of

$10,244 million, EBITDA of $4,310 million, and EBIT of $3,500 million.

Using those multiples and calculating the median of the enterprise

values, this method came down to the business enterprise value (BEV) of

$47,280 million of Monsanto (Table 1).

Table 1. Comparable Company Multiples Analysis of Monsanto BEV

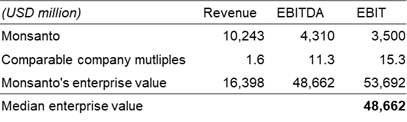

Methodology 2:

Comparable Acquisition Multiples

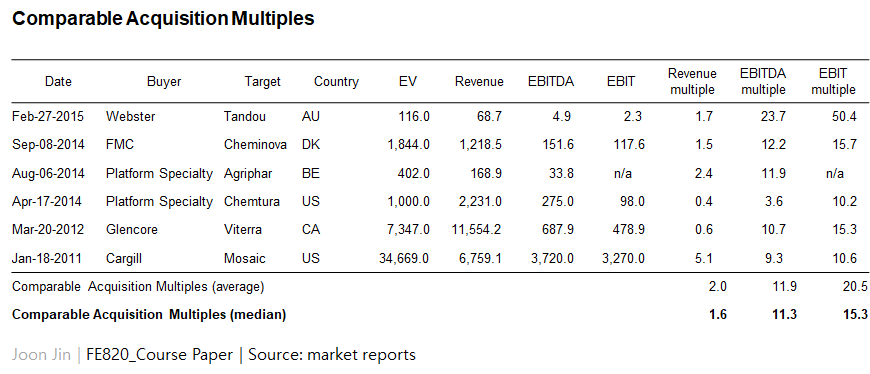

Although

the industry showed the changing landscape, there had not been many precedent

acquisitions for large target companies comparable to Monsanto before

2016. Due to this reason, I was only

able to gather acquisition data in the industry with smaller companies which

could still provide an insight for Monsanto’s deal. As seen in Exhibit 5,

the revenue multiples ranged from 0.4 and 5.1, and did the EBITDA multiples

from 3.6 and 23.7 and the EBIT multiples from 10.2 and 50.4. The median multiples of revenue,

EBITDA and EBIT were 1.6, 11.3 and 15.3, respectively. Using those

multiples and calculating the median of the enterprise values,

Monsanto’s BEV was $48,662 million (Table 2).

Table 2. Comparable Acquisition Multiples Analysis of Monsanto BEV

Methodology 3:

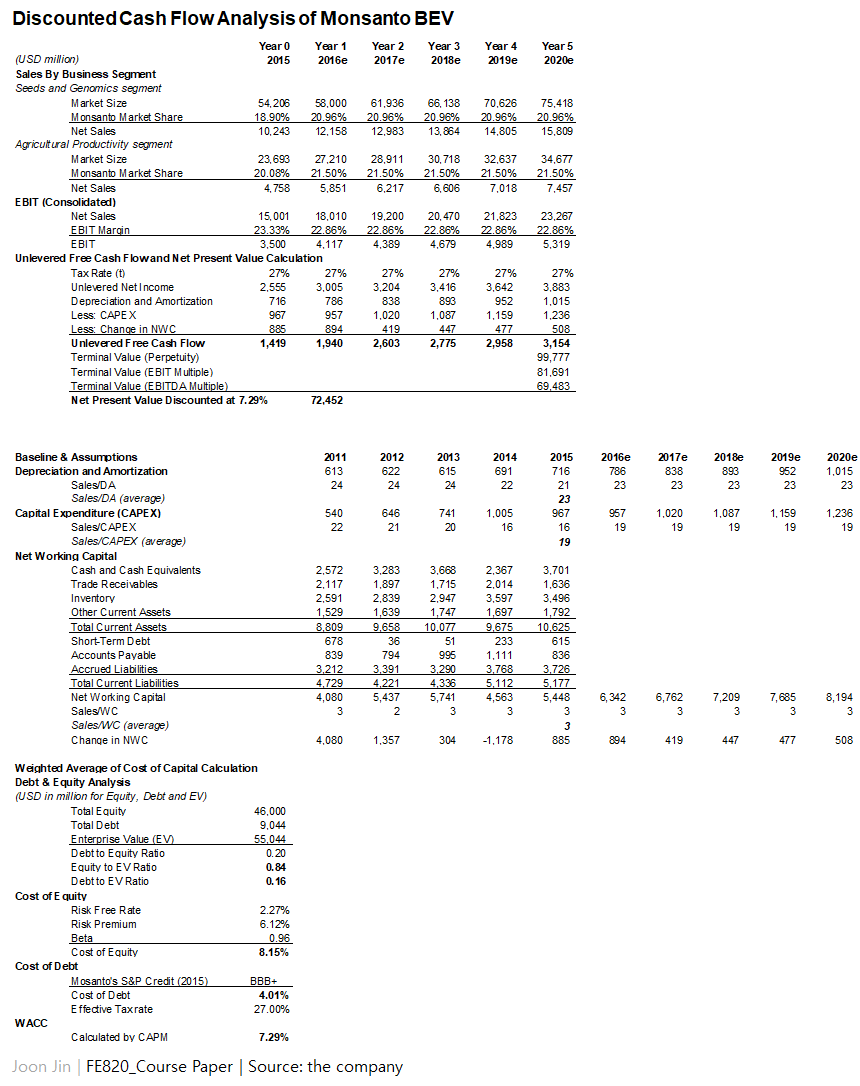

Discounted Cash Flow

Discounted cash

flow (DCF) is based on future estimation of a firm’s cash flow. It uses

detailed values taking specific factors into account, thus it can determine the

intrinsic value of a business. However there are significant amount of

assumptions in this methodology, so assumptions should be in correct ranges to

induce the right value.

DCF method is

composed of three major steps: Estimation of free cash flow (FCF),

calculation of cost of capital, and analysis of BEV. To forecast the FCF

of Monsanto, I first looked at the last five years’ earnings and cash flows of

the company. Monsanto showed $10+ billion of net sales in all years and

EBIT margin ranged from 20 to 25% (Exhibit 6).

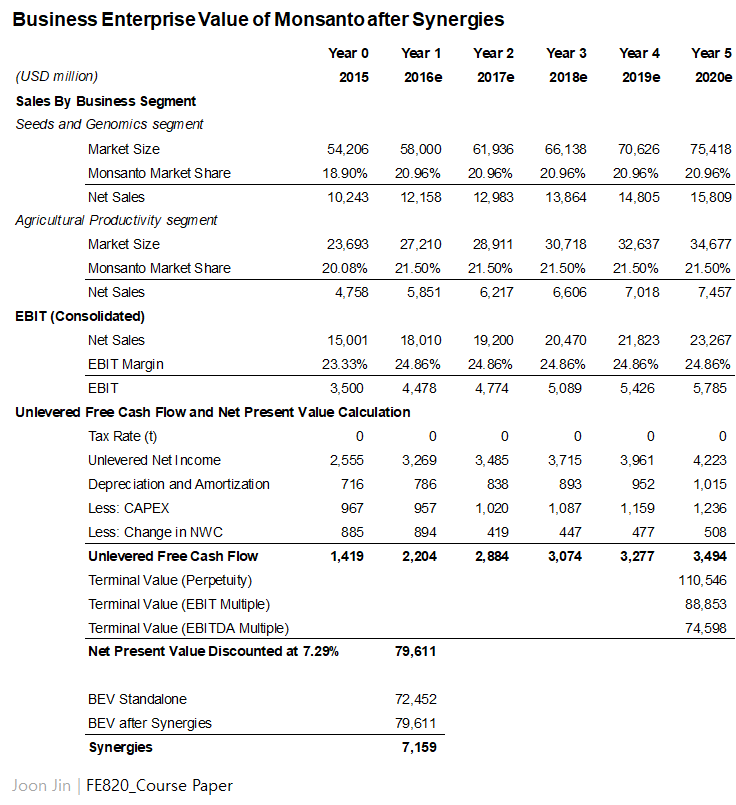

There were two business segments in Monsanto, Seeds and Genomics segment

and Agricultural Productivity segment. The former is basically a seed

business, and the latter is an agricultural chemicals business selling

herbicides (mostly RoundUp products).

Sales and EBIT of both segments are also shown in Exhibit 6. To estimate the future sales and EBIT, I used

those segments as baselines. Then historical market sizes of those

segments, i.e. global seed market and global herbicides market, in those years

were investigated to calculate the average market shares of Monsanto in each

segment (Exhibit 7, years 2011 to 2015).

Monsanto represented 20.96% and 21.50% of market shares in average in

seed and herbicides fields respectively. The market shares did not vary a

lot (with standard deviations of 0.01 and 0.02) and would remain as such in the

future, i.e. Monsanto’s market position would not be changed significantly as

the industry was dominated with a few players and new companies were to be

acquired by the players and also Monsanto kept investing in research and

development constantly on top of their current competitive edges as other

players. Therefore I decided to use the average market shares in each

segment to estimate the sales of Monsanto for the next five years by 2020

with the market sizes projected by reports (Research and Markets, 2017, Markets

and Markets, 2017, and Transparency Market Research, 2015). The results

are shown in years 2016 to 2020 in Exhibit 7 and Exhibit 8. Based on the sales estimation, EBIT was also

forecasted. EBIT margin was assumed to

stay similar in the future as the historical EBIT margins varied in a small

range. So I used average EBIT margin of last five years which is 22.86%

to forecast the next five. With the

effective income tax rate of Monsanto in 2015 which was 27%, the EBITs were

utilized to calculate the unlevered net income.

Next steps to

compute the FCF for the future were estimating depreciation and amortization,

capital expenditure (CAPEX), and working capital. Since they showed even

Ratio to Sales in the past, I envisioned that their investments in assets,

which is in turn reflected in depreciation and amortization and CAPEX, would be

grow at the same rate as sales. This was also applied to working capital

estimation based on the assumption that Monsanto had managed current assets and

current liabilities roughly according to the sales. Using all these figures based on ratio to

sales with the unlevered net income, I finally resulted in the forecasted

unlevered FCF of 2016 to 2020 (Exhibit 8).

Before moving

forward to have the present values in 2015 of the unlevered FCF, the terminal

value beyond 2020 should be added. In general, two methods are used to

get the terminal value of a firm: Perpetuity method and Multiple method. In perpetuity method, the terminal growth

rate of 4% was used which is a nominal value of the long-term gross

economic growth of the United States (source: OECD) then the terminal value

derived from this method was $99,777 million. With the discount rate

which will be described below, the net present value (NPV) of Monsanto’s free

cash flow and the terminal value was $80,960 million. In multiple method,

EBITDA multiple and EBITDA multiple of the comparable companies in Table 1 were

multiplied by estimated EBIT in 2020 here to calculate the terminal value of

the firm. Those were $69,483 million and $81,691 million with the average

value of $75,587 million. The NPV with

this terminal value represented $63,943 million. Two NPVs were averaged into $72,452 million

that is the final BEV of Monsanto using the DCF methodology (Exhibit 8).

Below is the summary of assumptions used for the DCF.

·

Sales forecast: Average of historical

market shares in each segments was applied to global market size forecasted by

market reports.

·

EBIT forecast: Average of historical EBIT

to sales ratio was applied to forecasted sales.

·

Depreciation and Amortization, CAPEX, and

NWC: Average of historical each values to sales ratio was applied to forecasted

sales.

·

Terminal growth rate in Perpetuity method:

The terminal growth rate of 4.0% was used which is a nominal value of

the long-term gross economic growth of the United States expected by OECD.

·

Terminal value multiples in Multiple

method: EBITDA multiple of 11.0 and EBIT multiple of 15.4 (in Table 1) were

multiplied by estimated EBITDA and EBIT in 2020 respectively.

As described above,

the discount rate was deployed here to calculate the present value of the

company. The cost of equity and cost of debt were used to compute the

weighted average of cost of capital (WACC). First, the market value of

equity and debt were analyzed. The market

value of equity equals to the market capitalization and Monsanto had $46

billion of market capitalization at the end of 2015. Per the market value

of debt, the book value of debt (total of short-term and long-term debt) was

used as a proxy and that was $9,044 million in 2015. The debt to equity ratio was 20%. The ratios

of equity and debt to enterprise value were 0.84 and 0.16

respectively.

Next, the cost of

equity was calculated. The risk free rate used here is 2.27% which is the

U.S. treasury bond rate in 2015. And the equity

risk premium in 2015 for the S&P 500 of 6.12% was used (Damodaran,

2019). Monsanto’s beta at the acquisition announcement was 0.96

(TheStreet, 2016). With those figures and the capital asset pricing model

(CAPM), the cost of equity of 8.15% was derived. Next, the cost of debt

was assumed with Monsanto’s credit rating. The S&P credit rating of

Monsanto was BBB+ in 2015. I was not able to obtain the bond rate of BBB+

for 2015 but the rates of BBB and A were 4.43% and 3.16% (source:

YChart). With the assumption of equal spread between ratings (I divided

the difference in rates of BBB and A by three (3) as there are two grades

between them: BBB+ and A-. The result value of 0.42% was used as the equal

spread, then 0.42% was subtracted from BBB’s rate of 4.43% to estimate the rate

of BBB+), the bond rate of BBB+ was computed and resulted in 4.01% which is the

cost of debt used in this study. Using the effective tax rate of 27% as

described above and also with the weights of equity and debt, I finally derived

the WACC of 7.29%. Again, at this WACC

as the discount rate, the final BEV of Monsanto using the DCF methodology

represented $72,452 million.

Synergies and

Final Valuation

Estimating

synergies can be done with two key aspects: Cost savings and Sales

synergies. Generally it is implied that target company captures all the

values from synergies thus the acquisition price would reflect it.

Baseline of this study to start is the fact that Monsanto was a giant in seeds

market while Bayer was more inclined to chemical products. According to

the Bayer’s presentation to investors, they would have annual sales synergies

of ~$200 million targeted as of 2022 generated from broader product portfolio

and greater geographic footprint by combining sales forces and

infrastructure. Although this number represents a small portion of sales

sum of both companies which was $25,000+ million in the relevant segments, I

assumed there would be no synergies from sales since many of their product

portfolio, e.g. target crops and target regions, were overlapped at that time

and even cannibalization would be expected, so those synergies would be offset

in term of sales. Mckinsey & Company (2018) noted that three

dimensions should be taken into account to estimate the sales synergies, where,

how, and what to sell, but again I assumed those dimensions would be offset by

the factors above then would end up with just the additive effect not the

synergies.

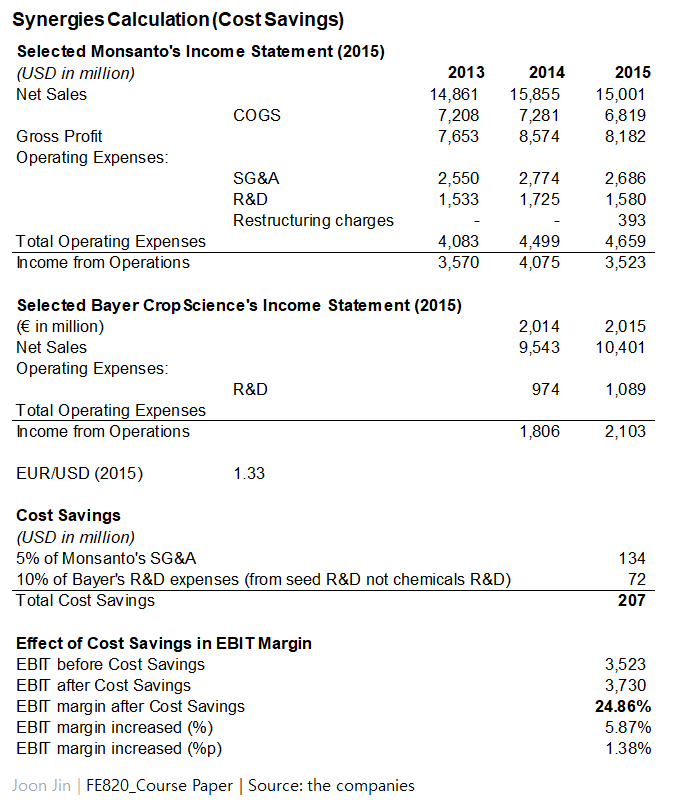

I rather assumed

those merits would flow into the cost saving synergies. Before beginning

calculation, I took a look at the Bayer’s investor presentation and they said

annual cost synergies of ~$1 billion targeted as of 2022. When I simply

applied 60% of this $1 billion to the EBIT of 2020 (as about 60~70% of $1

billion in cost savings would be achieved according to their data), the present

value of $10 billion was added by the DCF method (thus up to $82 billion of BEV

in DCF) . Generally acquirors are too optimistic to estimate the positive

effect of M&As, I decided not to follow this number but to estimate the

cost savings on my own. I first focused

on research and development (R&D) expenses.

The accounting rules for R&D expenses are different between US GAAP

and IFRS particularly with the fact that this acquisition is between the US and

the European ones, but I followed US GAAP rule, i.e. all the R&D costs are

regarded as expenses not assets. As noted, Monsanto possessed strong

competitiveness in crop biotechnology (and their seed products were generated

from it), I expected that Bayer’s R&D on seeds would harness Monsanto’s

capabilities. Bayer CropScience had ten

(10) R&D sites across the world.

Among them, five (5) sites were working on the seed research (Table

3).

Table 3. Bayer CropScience’s Global R&D Sites

I assumed those

five sites represents a half of total R&D expenses (five out of ten sites)

of Bayer CropScience and could save 10% of their R&D costs following the

acquisition. Exhibit 9 shows a part of Bayer CropScience’s income

statement in 2015 which was used to calculate the R&D cost savings. In result, total annual R&D expense of

$72.42 million (€54.45 million) was expected to

be saved. Another cost savings could come from selling, general and

administrative expenses (SG&A). The savings in SG&A can be

achieved by reducing redundant staff members, consolidating vendors, rent

savings, or merging infrastructures. However, it was difficult to find

specific data on this for the two companies, I assumed that 5% of Monsanto’s

annual SG&A would be saved which was $134.3 million (Exhibit 9).

In

total, about $206.72 million of annual cost savings could be achieved from

R&D and SG&A, and this represented 5.9% of EBIT of Monsanto in

2015. Therefore the EBIT margin would increased from 22.86% to

24.86%. I applied this EBIT margin of

24.86% back to DCF to re-estimate EBITs in the future then finally the BEV of

Monsanto from synergies was $79,611 million as opposed to the standalone firm’s

BEV of $72,452 million. Thus the synergies from this acquisition is

$7,159 million (Exhibit 10). Again, in this

study, Monsanto was assumed to capture all the values from synergies.

Finally I

calculated the common stock fair market value of Monsanto at the announcement

time. Monsanto’s interest bearing debt (IBD) of $9,044 million in 2015 was

subtracted from BEVs from three methodologies. Then to derive the common

stock fair market value, the synergies of $7,159 million were added to

pre-discount implied equity market value from comparable company multiples and

DCF methodologies, but not to comparable acquisition multiples as this

methodology already implies the synergies. Averaging the values from

three methods, the final common stock fair market value was $51,860

million. Considering the number of

shares outstanding of 481.4 million, the fair market value per share ended up

with the price of $108 per share (Exhibit 11, top) with the premium of 12.7% as

of 2015 or 21.0% as of May 2016 (the controlling premium was ignored in this

study).

Discussion and

Conclusion

The share price of $108 derived in

this study is less than the actual price Bayer offered which is $122 in May

2016 then increased to $128 in September 2016. As of one days before each

announcement, the premium in May and September offers are 40% and 44%. This discrepancy might be caused by what

methodologies they used to calculate Monsanto’s value. Now that Bayer’s

patents on two top-selling drugs from HealthCare business sector were to be expired

from 2023 and Bayer reportedly said the acquisition would cushion a possible

drop in pharmaceutical revenues, it is probable that they relied more on DCF

method valuing on earnings than the other two methods. When I put weights

for the result of DCF with 70% and 15% each for the other two methods, the

value actually converged to $62,149 million in common stock fair market value

and stock price of $129 per share (Exhibit 11, bottom) which is closed to the

actual price of the deal (under the assumption that all the synergies to be

paid to Monsanto). Another possible cause that drew the discrepancy is

the optimistic projection from Bayer for synergies. It was difficult to see how much synergies

they exactly assumed for the years in this study, but given the fact that they

expected $1.2 billion in annual synergies from both sales and cost targeted as

of 2022 and if this figure was reflected in the terminal value, the value of

the firm would increase significantly.

Otherwise, it could be a dawn of

big M&As in the agricultural biotechnology and chemicals field. A

partner at investment bank The Valence Group in 2017 was quoted as saying “15x

EBITDA really is the new 10x.” describing recent big M&As in chemical

industry. Along with that, Bayer’s offer price actually was 15.8x EBITDA

of Monsanto, and another big acquisition of the Swiss giant, Syngenta, by

ChemChina in 2017 with $43 billion purchase also had the EBITDA multiple of

17.5. Given that there had been few comparable M&As with the scale as

big as Monsanto or Syngenta before 2016 and that the EBITDA multiples in this

study were 11.3 (industry median), the mega trend of consolidation in this

business might have been forced buyers to pay more than they had used to do.

In 2019, in the wake of the finalization

of the deal in June 2018, the media say it is one of the worst corporate deals

so far (The Wall Street Journal, 2019). Unfortunately right after the

deal, glyphosate the chemical of Monsanto’s RoundUp herbicide brought pushbacks

to Bayer. Within weeks of the deal

closing, Bayer lost a lawsuit alleging glyphosate causes cancer. And the

effect might have been cascaded into Bayer’s pharmaceutical business. The consumer sentiment to a drug company, no matter

what business segment is involved, could be seriously jeopardized when it comes

to a safety issue. As noted above, the deal was aimed to cushion the

expiration of cash cow drugs’ patents of Bayer.

Now it turned out that the deal draws an unexpected ripple effect to the

conglomerate. It was noted above that

there would be cannibalization among Monsanto’s and Bayer’s products portfolio

from the acquisition in the CropScience segment. But I did not even

anticipate the negative effect would occur even against another business

segment. Nevertheless, putting aside the

fact if the glyphosate allegation was transparently shared with Bayer

management by Monsanto’s due diligence during the deal, this does not mean the valuation Bayer made

was significantly off target as the recent bad news are from external factors

which are hard to control for the company. We will see whether Monsanto’s

value of $63 billion would pay off or not to Bayer CropScience in next few

years.

Appendix:

Hindrances of Calculation

It was difficult

to gather all the exact figures from public sources, so I made lots of

assumptions. For example, in the calculation of cost of debt, I used the

bond rate of BBB+ based on the assumption of uniform spread between S&P

ratings since I could only find the bond rates of A and BBB as described

above. Another examples are terminal growth rate and cost saving

effects. Those were especially difficult

because the BEV was sensitively changed with those assumptions (see the

sensitivity analysis in Exhibit 12).

With the reasonable approaches I tried and searching bunch of reports

and articles for the industry, however, I made my best estimates in the study.

References

[Background

Industry and Market Information]

- The companies’ annual

reports and 10-Ks.

- “Nufarm: Looking for

chemistry”, Macquarie Research, March 2017.

- “Seeds Market: Global

Industry Trends, Share, Size, Growth, Opportunity and Forecast

2017-2022", Research and Markets, April 2017.

- “Herbicides Market by

Type (Glyphosate, 2, 4-D, Diquat), Crop Type (Cereals & Grains,

Oilseeds & Pulses, Fruits & Vegetables), Mode of Action

(Non-selective, Selective), and Region - Global Forecast to 2022”, Markets

and Markets, February 2017.

- “Global Herbicides Market

will Continue to Expand despite Growing Demand for Organic Farming”, Transparency

Market Research, November 2015.

- Ruth Bender, “How

Bayer-Monsanto Became One of the Worst Corporate Deals—in 12 Charts”, The

Wall Street Journal, August 2019.

- John Chartier, Alex Liu, Nikolaus Raberger and Rui Silva. “Seven Rules to Crack the Code on Revenue Synergies in M&A”, McKinsey & Company, October 2018.

[Sources in

Valuation]

- Damodaran, Aswath, Equity

Risk Premiums (ERP): Determinants, Estimation and Implications – The 2019

Edition (April 14, 2019). Available at SSRN: https://ssrn.com/abstract=3378246

or http://dx.doi.org/10.2139/ssrn.3378246

- “Monsanto (MON)

Highlighted As Momo Momentum Stock”, TheStreet, May 2016.

- OECD: http://www.oecd.org/

- Macrotrends: https://www.macrotrends.net/

- Stockcrow: https://stockrow.com/

- Gurufocus: https://www.gurufocus.com/

- YCharts: https://ycharts.com/

- StreetInsider.com: https://www.streetinsider.com/

Exhibit 1.

Exhibit 2.

Exhibit 3.

Exhibit 4.

Exhibit 5.

Exhibit 6.

Exhibit 7.

Exhibit 8.

Exhibit 9.

Exhibit 10.

Exhibit 11.

Exhibit 12.